What Is the Kelly Criterion?

Introduction

The Kelly Criterion is a mathematical formula used to calculate an optimal stake size when a bettor believes there is a measurable edge. Its main purpose is to help maximise long-term bankroll growth while avoiding unnecessarily large stakes. In sports betting, the method is based on probability estimates, available odds and expected value, giving bettors a structured approach to bankroll management.

Key features of the model:

- Calculates the percentage of the available bankroll that may be used for a specific bet, based on the perceived edge and the odds.

- Requires a realistic probability estimate for the outcome being considered.

- Helps reduce the risk of overstaking during losing runs or uncertain betting periods.

- Is commonly used in long-term betting strategies where risk exposure must be controlled.

- Can be adjusted by using a fractional approach, such as half Kelly, for more conservative bankroll management.

- Requires discipline and consistency, especially when estimating probabilities and applying the formula.

This model offers a structured way to decide stake size, with the central goal of supporting sustainable bankroll growth over time. It does not guarantee that losses will be avoided, but it is designed to help limit the risk of ruin and encourage more disciplined decision-making. It is best suited to bettors who can work with reliable probability estimates and want to approach long-term betting results more analytically.

How the Kelly Criterion Formula Is Calculated

Examples with Real Numbers

Optimal Stake Formula

Calculates what percentage of the bankroll may be staked when a bet has measurable value.

Long-Term Bankroll Growth

The goal is disciplined bankroll growth through probability-based staking.

Risk Control

It helps limit overstaking when betting with a fixed bankroll.

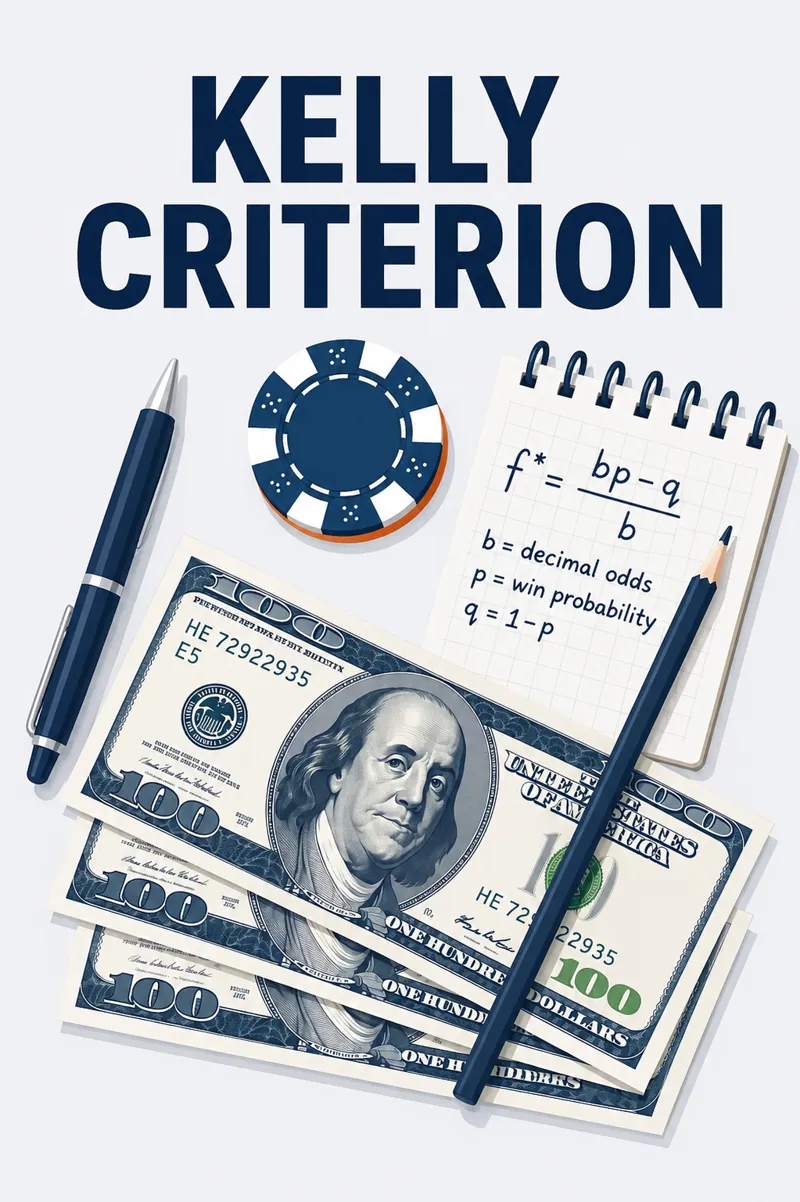

The Kelly Criterion is a mathematical staking model that calculates the optimal percentage of a bankroll to stake when a bet appears to offer positive expected value. It is based on the bettor’s estimated probability of success and the available odds.

The formula is:

f = (bp - q) / b, where:

- f – the percentage of the bankroll to stake; a value above 0 suggests a positive-edge bet, while a value below 0 means the bet should be avoided

- b – the net profit per unit staked (for example, with odds of 3.00, b = 2); this is the profit after subtracting the original stake

- p – the probability of success in decimal form; this is the key estimate that directly affects the calculation

- q – the probability of failure (1 - p); the higher this number is, the greater the risk of losing the bet

For example, if a bettor estimates that a team has a 60% chance of winning and the available odds are 2.50, then:

- b = 2.50 - 1 = 1.5; this is the profit for each unit staked

- p = 0.60, q = 0.40; these probabilities must come from a realistic betting assessment or statistical model

- f = (1.5 × 0.60 − 0.40) / 1.5 = (0.90 − 0.40) / 1.5 = 0.50 / 1.5 ≈ 0.33; in this case, the full Kelly stake would be about 33% of the bankroll

In this example, the Kelly Criterion suggests a full Kelly stake of approximately 33% of the bankroll. In practical sports betting, many bettors use a fractional version of this amount to reduce volatility.

Summary table with Kelly Criterion examples:

| Event | Odds | Win Probability (p) | Net Profit (b) | Kelly % | Decision |

|---|---|---|---|---|---|

| Team A vs Team B | 2.50 | 60% (0.60) | 1.50 | 33% | Consider staking |

| Match X vs Match Y | 3.00 | 40% (0.40) | 2.00 | 10% | Consider staking |

| Event C | 2.20 | 45% (0.45) | 1.20 | -0.8% | Skip |

Important: The formula depends on a realistic and accurate probability estimate. If the estimated probability is wrong, the calculation can produce inappropriate stake sizes and increase the risk of unwanted losses.

In practice, many bettors use fractional Kelly, such as half Kelly, to reduce volatility and smooth out bankroll swings.

The approach is used by analytical sports bettors, but it requires strict risk management and a careful assessment of value before each betting decision.

Examples of Kelly Criterion in Sports Betting

The Kelly Criterion is a mathematical model used to calculate stake size based on expected value, odds and the estimated probability of success. The examples below show how the strategy can be applied across different sports betting scenarios.

A bettor estimates that a football team has a 55% chance of winning, while the available odds are 2.10. Using the Kelly Criterion, the optimal full Kelly stake is approximately 14% of the bankroll. This suggests positive expected value, provided the probability estimate is realistic.

In a tennis match, a bettor believes the favourite has a 70% chance of winning, while the available odds are 1.80. The calculation gives an optimal full Kelly stake of about 32.5% of the bankroll, which indicates a strong mathematical edge if the probability assessment is accurate.

In a basketball match, the probability of success is estimated at 50%, with odds of 2.00. In this case, the strategy points to a zero stake, because the bet does not offer positive expected value after applying the formula.

For a multiple bet involving several selections, the method can be used to assess the combined probability and the overall stake size. With an estimated probability of 35% and total odds of 3.50, the calculation produces a Kelly stake of approximately 9% of the bankroll.

These examples show how the Kelly Criterion can support more structured staking decisions when a bettor has a measurable mathematical edge. The model depends heavily on accurate probability estimates and is best suited to a disciplined, analytical approach to sports betting.

Full Kelly vs Fractional Kelly

This bankroll management model, known as the Kelly Criterion, aims to support long-term bankroll growth by calculating a stake size based on expected value. It is usually applied in two main ways: full Kelly and fractional Kelly, with each approach offering a different balance between growth potential and risk control.

With full Kelly, the bettor stakes the entire percentage suggested by the formula. This approach targets maximum long-term bankroll growth, but only works well when the probability estimates are accurate. At the same time, it can create large bankroll swings, especially during losing runs.

Fractional Kelly uses only a fixed portion of the full Kelly stake, such as 50% or 25%. This more conservative approach helps reduce volatility and is often more practical when probability estimates are uncertain, although it also limits potential growth.

If the bettor’s probability assessment is inaccurate, applying the full Kelly stake can lead to rapid losses and unstable results. For this reason, the method requires a high level of confidence in the analysis and a solid understanding of probability.

Fractional Kelly provides more flexible bankroll management. It allows bettors to adapt staking to different risk profiles and can reduce the psychological pressure that comes with large stake sizes and short-term variance.

In summary, full Kelly may be suitable when the bettor has strong confidence in the probability estimate and wants to maximise long-term growth, while fractional Kelly is usually preferred for a more cautious staking strategy. The right choice depends on risk tolerance, bankroll size and the quality of the betting analysis.

Advantages of the Kelly Criterion Strategy

The Kelly Criterion provides a mathematically structured approach to bankroll management in sports betting. It is designed to help optimise long-term bankroll growth by linking stake size to expected value, odds and the bettor’s estimated probability of success.

The method focuses on maximising expected long-term growth rather than choosing stake sizes at random. This makes it useful when assessing bets that appear to offer positive expected value.

The approach combines growth potential with risk control. Because stake size is linked to both the perceived edge and the probability of success, it can help reduce exposure when the advantage is small or uncertain.

The model is based on a clear mathematical framework, which gives bettors a more disciplined way to evaluate staking decisions. This can be especially helpful for users who prefer a probability-based approach instead of emotional or impulsive betting.

The strategy can be adapted to different betting markets, odds formats and probability estimates. This flexibility allows it to be used across various sports betting scenarios, as long as the bettor can make realistic assessments.

By calculating a recommended stake size, the Kelly Criterion helps limit excessive staking. This is important for bankroll protection, especially when betting through licensed South African betting operators where disciplined stake control remains essential.

In summary, the Kelly Criterion offers a structured and measurable staking method for bettors who work with reliable probability estimates. It is most useful as part of a long-term betting strategy where risk, value and bankroll discipline are all considered before placing a bet.

Disadvantages and Real Risks

The Kelly Criterion is based on mathematical calculations designed to optimise staking decisions. Although it can be useful for structured bankroll management, the strategy has clear limitations and practical risks that bettors should understand before applying it.

The effectiveness of the method depends heavily on a realistic and accurate probability estimate. If the estimate is wrong, the formula can suggest disproportionate stake sizes, which may weaken the overall betting strategy.

Although the model aims to support long-term bankroll growth, it does not guarantee stable short-term results. Losing runs can still happen, and the bankroll may experience significant fluctuations even when the method is applied correctly.

Applying the approach requires calculation accuracy and analytical thinking. For some bettors, this can be difficult in real time, especially without reliable tools or a clear process for estimating probabilities.

Using the full stake size recommended by the formula can lead to large bankroll swings. This is why many bettors prefer fractional Kelly, which reduces exposure by using only part of the calculated stake.

The model assumes that stake sizes can be applied precisely and that the selected market remains available at the expected odds. In real sports betting markets, operator limits, odds movement and stake rounding can reduce the practical effectiveness of the approach.

In summary, the Kelly Criterion is a structured and logical staking model, but it requires accurate estimates, a long-term view and careful bankroll control. It should not be treated as a guaranteed profit system and is best used with caution, discipline and realistic expectations.

Frequently Asked Questions (FAQ)

The Kelly Criterion is a mathematical staking model used to calculate an optimal bet size with the aim of supporting long-term bankroll growth. It considers the estimated probability of success and the relationship between risk and potential return.

The formula is f = (bp – q) / b, where:

f is the fraction of the bankroll to stake,

p is the probability of success,

q is the probability of failure (1 - p),

b is the net profit per unit staked.

The calculation requires a realistic probability estimate and accurate odds information.

The method supports structured bankroll management by linking stake size to probability, odds and expected value. It can help bettors avoid random stake sizing and reduce the risk of excessive exposure when the perceived edge is small.

Yes. The method depends on an accurate probability estimate, which can be difficult in real sports betting markets. If the estimate is wrong, the formula may suggest a stake that is too large, increasing bankroll volatility and overall risk.

It can be useful for learning structured stake management, but it is usually better suited to bettors who understand probability, odds and bankroll control. Beginners may find fractional Kelly easier to apply because it reduces risk compared with full Kelly staking.

The Kelly Criterion can support more disciplined long-term bankroll management when used with realistic expectations and accurate probability estimates. However, it does not remove risk, does not guarantee profit and should not be treated as a guaranteed betting system.