What is the Kelly Criterion?

Introduction

Kelly Criterion is a mathematical formula used to calculate the optimal bet size when a bettor believes there is an edge. Its main idea is to maximise long-term bankroll growth while avoiding excessive exposure. The strategy is based on probabilities and expected value, giving Indian users a structured way to manage betting funds with clearer risk control.

Main characteristics of the model:

- Defines the percentage of available bankroll to use for a specific bet, based on the edge and the odds.

- Requires an accurate estimate of the probability that the bet will be successful.

- Helps reduce the risk of excessive losses during a run of unsuccessful bets.

- Used mainly in long-term strategies where bankroll exposure is controlled.

- The approach can be adjusted through fractional Kelly, such as half Kelly, for more conservative bankroll management.

- Requires discipline and consistency, especially when working with probabilities and calculations.

This model provides a structured approach to bet sizing, with the main goal of sustainable bankroll growth. The method does not remove the risk of losses, but it is designed to reduce the risk of bankroll ruin and support more disciplined fund management. It is most relevant for users who work with credible probability estimates and want to approach long-term betting decisions with clearer mathematical control.

How the Kelly Criterion formula is calculated

Examples with real numbers

Formula for optimal percentage

Defines what percentage of the bankroll should be staked when a bet has value.

Maximising growth

The aim is long-term bankroll growth through optimised bet sizing.

Risk control

Helps prevent excessive risk when betting with a limited bankroll.

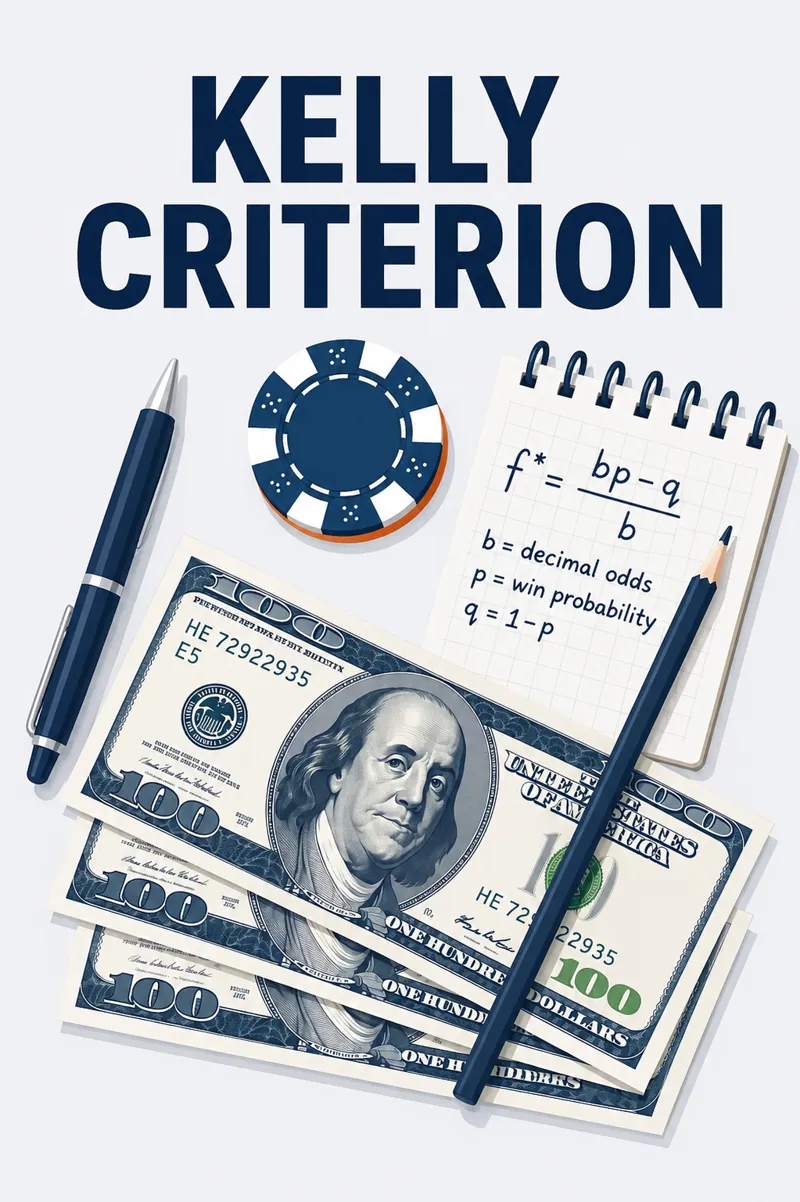

Kelly Criterion is a mathematical model that calculates the optimal percentage of the bankroll to stake when a bet has value (value bet). It is based on the probability of success and the available odds.

The formula is:

f = (bp - q) / b, where:

- f – the percentage of the bankroll to stake; a value above 0 indicates a positive-value bet, while a value below 0 means the bet should be skipped

- b – the net profit per unit staked (for example, at odds of 3.00, b = 2); it represents the profit after subtracting the original stake

- p – the probability of success in decimal form; this is a key component, and its accuracy directly affects the effectiveness of the strategy

- q – the probability of failure (1 - p); the higher it is, the higher the risk of losing the bet

For example, if a bettor estimates that a team has a 60% chance of winning and the odds are 2.50, then:

- b = 2.50 - 1 = 1.5; this is the profit for every unit staked

- p = 0.60, q = 0.40; the probabilities are based on prior analysis or statistical evaluation

- f = (1.5 × 0.60 − 0.40) / 1.5 = (0.90 − 0.40) / 1.5 = 0.50 / 1.5 ≈ 0.33; in this case, the calculated stake is around 33% of the bankroll

Therefore, under the Kelly Criterion, the suggested stake is around 33% of the bankroll in this specific example.

Summary table with Kelly Criterion examples:

| Event | Odds | Probability of success (p) | Net profit (b) | Kelly % | Recommendation |

|---|---|---|---|---|---|

| Team A vs Team B | 2.50 | 60% (0.60) | 1.50 | 33% | Consider |

| Match X vs Match Y | 3.00 | 40% (0.40) | 2.00 | 10% | Consider |

| Event C | 2.20 | 45% (0.45) | 1.20 | -0.83% | Skip |

Important: The formula relies on a realistic and accurate probability estimate. If the estimate is wrong, the calculation can lead to poor stake sizing and unwanted losses.

In practice, bettors often use fractional Kelly (for example, half of the calculated percentage) to reduce volatility and bankroll swings.

The approach is popular among sports analysts and experienced bettors, but it requires strict risk management and careful value assessment before each betting decision.

Examples of use in sports betting

Kelly Criterion is a mathematical model for calculating optimal bet size based on expected value and the probability of success. The examples below show how the strategy works across different types of sports events.

A bettor estimates that a football team has a 55% chance of winning, while the operator offers odds of 2.10. According to the method, the optimal stake is approximately 14% of the bankroll. This indicates positive expected value and supports a more disciplined long-term approach.

In a tennis match, the bettor believes that the favourite has a 70% chance of winning, while the available odds are 1.80. The calculation shows that the optimal stake is around 32.5% of the bankroll, which points to a value-based decision under the model.

In a basketball match, the probability of success is estimated at 50%, while the odds are 2.00. In this case, the strategy gives a zero stake, because there is no expected value. This shows how the approach helps avoid bets without a mathematical edge.

For an accumulator made up of several events, each with its own assessed value, the method can be used to calculate the overall value and the optimal stake percentage. With an estimated probability of 35% and combined odds of 3.50, the calculation gives a stake value of around 9%.

These examples show that Kelly Criterion can support bettors when optimising bet size, provided there is a clear mathematical edge. The model requires accurate probability estimates and is better suited to an analytical approach to betting.

Full Kelly vs Fractional Kelly

This bankroll management model, known as the Kelly strategy, aims to optimise long-term returns by calculating the right stake size in relation to expected value. It has two main forms: full and fractional, with each offering a different approach to risk management.

With the full version of the method, the entire calculated share of the bankroll is staked according to the formula. This allows maximum bankroll growth when the probability estimates are accurate. At the same time, this approach can lead to significant swings in bankroll value.

The fractional version of the strategy uses a fixed portion of the full Kelly value — for example 50% or 25%. This more conservative model reduces volatility and is more suitable when estimates are less certain, but it also limits growth potential.

With inaccurate forecasts, using the full version of the model can lead to quick losses and instability. For that reason, the approach requires strong confidence in the analysis and a clear understanding of probabilities.

The fractional approach provides more flexible bankroll management. It supports different risk profiles and reduces psychological pressure on the bettor during losing runs or uncertain market conditions.

In summary, the full version of the method is suitable when there is high confidence in the estimates and a focus on maximum return, while the fractional approach is preferred for a more conservative strategy and incomplete information. The choice between the two depends on risk tolerance and the quality of the analysis.

Advantages of the strategy

The Kelly Criterion strategy provides a mathematically grounded approach to bankroll management in betting. It is designed to optimise bankroll growth over the long term and is used in different areas, including financial markets and sports betting.

The approach focuses on maximising expected logarithmic growth of capital. This makes it a useful tool when assessing bets with positive expected value.

The method combines aggression and control by limiting the risk of complete bankroll loss. Bet size is calculated in proportion to expected value and probability, which reduces exposure when the edge is weaker.

The model has a solid mathematical foundation and is widely recognised in probability theory and finance. This is why it is often used by professional analysts and investors.

The strategy can be adapted to different bet types and probability estimates. This flexibility supports its use in traditional betting decisions as well as more complex investment scenarios.

By calculating the optimal stake size, the approach limits excessive risk that can arise from impulsive decisions or from using more aggressive staking systems without clear probability control.

Overall, this model provides a structured and measurable mechanism for bet sizing, which is useful for users who rely on credible probability estimates. It fits a long-term strategy with controlled risk and a more analytical view of market behaviour.

Disadvantages and real risks

The approach known as Kelly Criterion is based on mathematical calculations designed to optimise bet sizing. Despite its precision, the strategy has real limitations and practical risks that need to be considered before use.

The main effectiveness of this method depends on a realistic and accurate estimate of probabilities. An inaccurate calculation leads to disproportionate stakes, which weakens the overall strategy.

Although the model aims to maximise long-term growth, it does not guarantee short-term stability. This can result in fluctuations in results and temporary losses.

Applying this approach requires calculation accuracy and analytical thinking. For some bettors, this can be a barrier in real-time betting, especially without suitable tools.

Using the full value suggested by the formula can lead to significant bankroll swings. For this reason, bettors often prefer fractional versions of the strategy to limit exposure.

The model assumes strong liquidity and the ability to place exact stake amounts. In real betting conditions, platform limits and stake rounding can reduce the full efficiency of the approach.

Overall, Kelly Criterion is a structured and logical model for bankroll management, but its use requires precise estimates, a long-term view and an understanding of market conditions. The method is not universal and should be applied with care and adjustment to real betting conditions.

Frequently Asked Questions (FAQ)

Kelly Criterion is a mathematical model used to calculate optimal bet size with the goal of long-term bankroll growth. The strategy considers the probability of success and the available risk-reward ratio.

The formula is f = (bp – q) / b, where:

f is the proportion of bankroll to stake,

p is the probability of success,

q is the probability of failure (1 - p),

b is the net profit per unit staked.

The calculation requires a realistic probability estimate and accurate odds information.

The approach supports structured bankroll management by aiming for maximum geometric growth over the long term. It also helps limit the risk of bankroll ruin by avoiding excessive stake sizes.

The method relies on a precise estimate of probabilities, which is difficult in real betting conditions. If the assumptions are wrong, the formula can suggest an overly large stake, increasing volatility in results.

The strategy requires probability skills and basic knowledge of risk management. For that reason, it is more suitable for users with some betting experience than for complete beginners.

When applied with realistic expectations and accurate probability estimates, the approach supports more consistent bankroll growth over time. It still does not remove risk and does not guarantee any specific result.